Purpose

The purpose of this post is to outline the key functions of the Permanent Loan in CREModels development models. These features should be universal across all development models unless noted otherwise. We also cover how the metrics and values within the Permanent Loan portion of Financing are calculated and used.

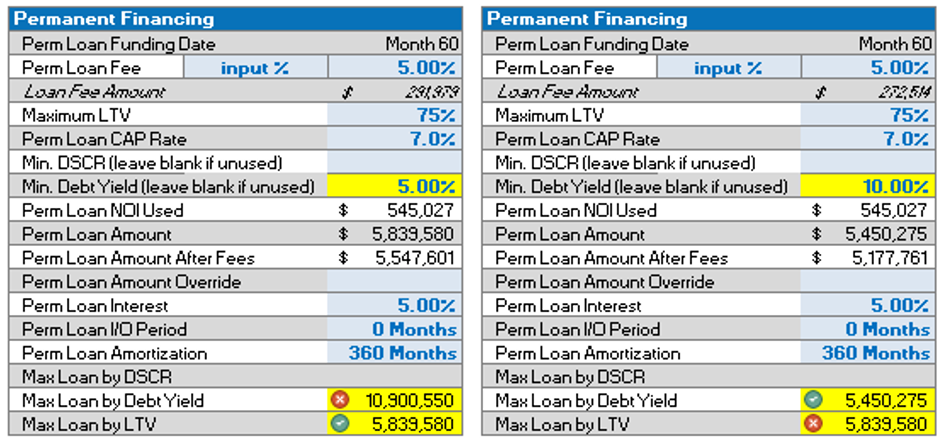

Permanent Financing

This section of the model allows user to model the permanent loan that will commence following the term of the construction loan. While a construction loan is a temporary loan used to cover costs during construction, the permanent loan pertains to the long-term financing of the property.

A) Perm Loan Fee

The perm loan fee cells allow the user to input the loan fee as a percentage of the loan amount or as a dollar amount. Cell P28 allows users to select between an input percentage and a dollar amount. Input percentage will calculate loan fee as a percentage of the Max Loan Amount displayed in cells Q41-Q43. Dollar amount will utilize the dollar amount inputted as the total loan fee amount. Cell Q28 allows users to add their desired loan fee percentage if input percentage is selected or the total amount of the loan fee if input dollar is selected in cell P28.

B) Maximum LTV

The LTV input allows users to select the LTV percentage amount that will be financed with the permanent loan. The remaining loan amount will be funded by equity. The model utilizes Perm Loan NOI divided by the Perm Loan CAP Rate to determine the total amount needed by both equity and debt. The model then takes the total amount multiplied by the Max LTV to calculate the Max Loan to LTV in cell Q43.

C) Cap Rate

A cap rate is the ratio of the net operating income to the properties asset value. This cell allows users to input a cap rate that the model will use determine the loans LTV amount in dollars. The model will divide the Perm Loan NOI by the cap rate and then multiply by the LTV percentage to determine the loan amount.

D) Min. DSCR

The debt service coverage ratio (DSCR) is a measure of the cash flow available to pay current debt obligations. A commercial lender will use the DSCR to determine the maximum loan amount or whether the property can sustain the debt it is incurring. The user has the option to enter the Min DSCR required by the lender. If a value is entered for Min. DSCR, the model will determine the Loan Amount based on the lesser of the calculated Max Loan by DSCR and the calculated Max Loan by LTV. The model will display a green check mark next to the loan amount being utilized. If the user does not have a minimum DSCR then this cell should be left blank.

E) Min. Debt Yield

Debt yield is a property’s NOI as a percentage of the total loan amount calculated as debt yield equals NOI divided by the loan amount. Many multifamily lenders require a minimum debt yield in order to approve a loan. One can use the minimum debt yield to determine the max loan amount by rearranging the formula to loan amount equals NOI divided by minimum debt yield. For example, if the minimum debt yield is 12% and the properties NOI is $200,000 annually, then you can calculate the max loan amount of $1,666,667 ($200,000 / 12% = $1,666,667). The model will calculate the Max Loan by Debt Yield if any percentage is inputted in cell Q33 and display this amount in cell Q42. If the Max Loan by Debt Yield in cell Q42 is greater than the Max Loan by LTV in cell Q43 then the model will use the Max Loan by LTV. If the Max Loan by Debt Yield is less than the Max Loan by LTV then the model will use the Max Loan by Debt Yield. The model will display a green check mark next to the loan amount being utilized. If the user does not have a minimum debt yield, then cell Q33 should be left blank.

F) Perm Loan Amount Override

This cell allows users to manually override the formulas in the model and manually determine the amount of the permanent loan. If an input is placed in this cell, the model will disregard the loan amount determined by formulas in cell Q43 and instead utilize the inputted loan amount. If the user does not wish to manually input a loan amount, then this cell should be left blank.

G) Loan Interest

This cell allows users to input the interest rate on the loan.

H) I/O Period

This cell allows users to select if any interest only period should be included in the loan. An interest only loan period is an agreed-upon span of time in which a borrower only pays interest on the loan and no principal.

J) Loan Amortization

This cell allows users to input their desired amortization duration. Amortization in real estate refers to the process of paying off your loan with regular monthly payments towards principal and interest.